With the major stock indexes hitting all-time highs and bond yields near all-time lows, it seems like a good time to talk about one of my favorite investing topics—diversification. It’s an important subject. Because when we think about building multi-asset portfolios, one of the things we try to do is reduce the effect of market volatility (those inevitable and sometimes dramatic ups and downs).

One of the best ways to do that is to build as much diversification as possible into the portfolio. This way, whatever the markets may do in the short- term, you’ll have a better chance of staying invested over the long haul, increasing the likelihood of reaching your goals. Now let’s consider some real world examples.

If you’ve been watching financial TV or reading the newspapers, you may have noticed the verbal drubbing bonds have been enduring lately. Indeed, the demise of bonds is a hot topic today. It’s actually a dramatic turn of events because as recently as February 2013, clients wanted to “reduce risk” in their portfolios in 2012 by moving to bonds.

How quickly things change. When I speak to investors these days, many ask why they should own any bonds at all? Even Warren Buffett got into the act in early May when he declared “Bonds are a terrible investment right now.” I’m not one to argue with Mr. Buffett, but , we believe bonds will continue to play an important diversifying role in balanced portfolios.

Now we’re not saying that you should buy and hold a portfolio full of 30-year Treasuries which as of this writing on May 28, 2013, were yielding 3.31%. But we believe owning an actively managed global bond portfolio makes sense today. As Jeff Hussey, Russell’s chief investment officer of fixed income, recently wrote, “skilled active managers have the opportunity to build yield into bond portfolios if rates rise gradually (as the Fed has indicated it aims to achieve) in ways that don’t jeopardize the traditional role of the bond component of an overall portfolio: moderating equity volatility and providing income.”

What’s more, economist, Mike Dueker (who worked as an economist for the St. Louis Fed for 17 years before joining Russell in 2008) believes the Fed will hold interest rates at extraordinarily low levels until 2015. The Fed has said it won’t consider raising rates until real inflation reaches 2.5% and the unemployment rate hits 6.5%.3 If Mike’s view is correct, we do indeed have some distance to go before unemployment falls to that level, which is why we don’t see short-term interest rates rising in the near-term.

In regard to longer term interest rates, most economists are looking at the yield of the 10-year Treasury to be around 2.3% by year-end. That projection is a modest increase from where that rate is today—2.15%. So we are looking at short-term rates to stay at or near zero and the yield on the 10-year Treasury to modestly increase by year-end.

We don’t believe it’s a good time to give up on bonds. Nor do we think it’s a good time to reach for yield. If you find a bond with a yield that sounds too good to be true, it probably is. The best thing investors can do right now is to understand the role bonds play in a globally diversified portfolio.

Recent headlines about the U.S. equity markets continuing to hit and surpass their previous highs have led many investors to question what’s going on with their diversified portfolios.4 Why haven’t they kept pace with the markets? Investors naturally want all of the pieces of their portfolio to move upwards—preferably all the time—but that is not always the case.

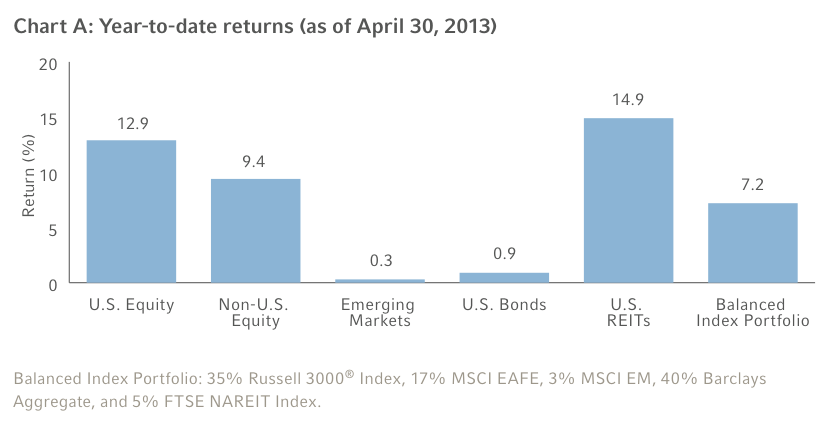

In fact, when diversification is at its best, there will always be parts of an overall portfolio that lag while other parts excel (see Chart A). That’s because diversification, although it doesn’t assure profit or protect against loss in declining markets, is designed to be a powerful response to the fact that nobody has perfect knowledge of what tomorrow will bring.

Those investors who knew on January 1, 2013, that U.S. stocks would be the leading asset class through the first quarter of the year could have positioned their portfolio accordingly. But those hypothetical investors with flawless foresight don’t exist.

To address this uncertainty, a diversified portfolio may include modest allocations to asset classes that have historically moved in different patterns. So you might construct a portfolio that had quite a bit more than just U.S. stocks. For instance, you’d also want to include non-U.S. stocks (developed and emerging), fixed income (U.S. and non-U.S.), real estate, commodities, etc. Such combinations are meant to help create a performance experience that is ideally directionally correct and never spectacularly wrong

Regarding the fact that many U.S. equity indexes have touched and passed their previous highs (as of this writing!), let’s take a longer-term view of how diversification has performed from the prior highs of these indexes. In the exhibit below (Chart B), note that a hypothetical diversified index portfolio has seen quite a strong return path from its prior high of October 2007.

What’s more, the same factors that worked against a diversified portfolio in the first quarter of 2013 were additive over this longer time period. As Erik Ristuben, Russell’s chief investment strategist, stated the other day, “You know your portfolio is diversified when three of your 11 holdings are disappointments in a given period.”

Need more convincing? The late, great investor and author Peter Bernstein used to say,

“You’re not really diversified unless you own something you’re uncomfortable with.”

It’s something to keep in mind the next time you’re cursing those underperforming asset classes in your portfolio.

Filed under: Misc, Uncategorized | Tagged: bonds, diversification, financial planning, reduce risk | Leave a comment »